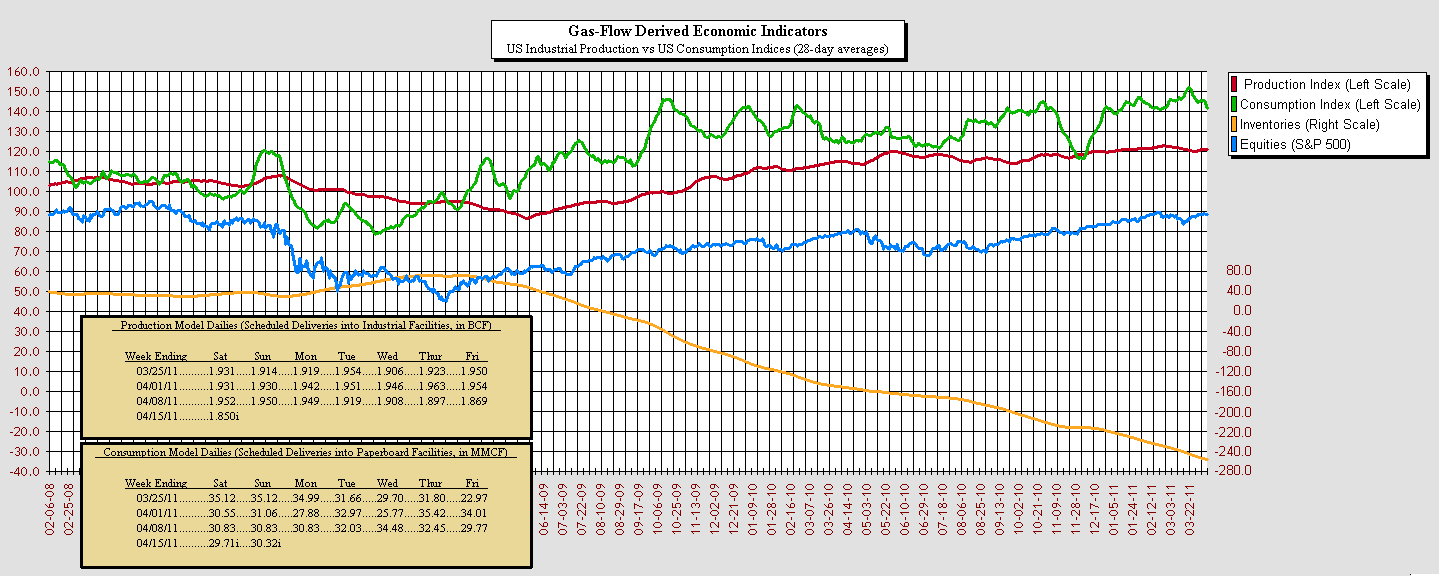

The US Industrial economy advanced slightly last week (if pipeline scheduling is correct), while consumer spending continued to fade.

The US Industrial economy advanced slightly last week (if pipeline scheduling is correct), while consumer spending continued to fade.The Production Index (In terms of its 28-day moving average of gas-flow scheduling into US industrial facilities) moved higher in the latest week (third gain in four weeks) at 121.8 (vs last weeks revised 121.4). In its dailies (raw, non-seasonally adjusted flows) the week started soft, firmed midweek, then ended somewhat flat.

The Consumption Index eased again (5th down-week in a row), slipping to 134.5 (from last weeks 135.4). In its dailies the week was choppy but overall soft.

The Inventories measure (the cumulative weekly difference between the Production Index and the Consumption Index) again continued in its long-term decline.

Food Group scheduling (see "Part 8" posts on the Investor Village site) is of great concern... the measure has been ominously strengthening as of late, rising to near levels not seen since the January/February 2009 recessionary-bottom. Such activity is strongly indicative of deep consumer mistrust in the economy (probably the reason for that 5-week decline in the consumption index). The Food group has a contra-relationship with consumption, and gains to the measure historically have tended to coincide with weakness in consumer spending.

The state of the recovery for the moment is very uncertain... almost akin to a gas leak in the basement that has yet to ignite (where you hope you can get the gas shut off and basement aired out before something produces a spark). Hopefully one of those sparks won't be the saber-rattling between Democrats and Republicans regarding budgeting and threatened government default, or the forthcoming end of QE2 (second round of quantitative easing).

(My preference would be to see to see at least a meek "QE-3"... perhaps 1/2 of QE-2 (though it will continue to pressure the dollar)... and to see the White House take default off the table by executive order.)

But for the moment... the recovery continues to appear supported by the lead in the Consumption Index over the Production Index, and continuing declines in the Inventories measure... assuming no sparks! Once past the Easter holiday we are really going to need to see consumer spending reaffirm itself to keep fundamentals in place.

-Robry825