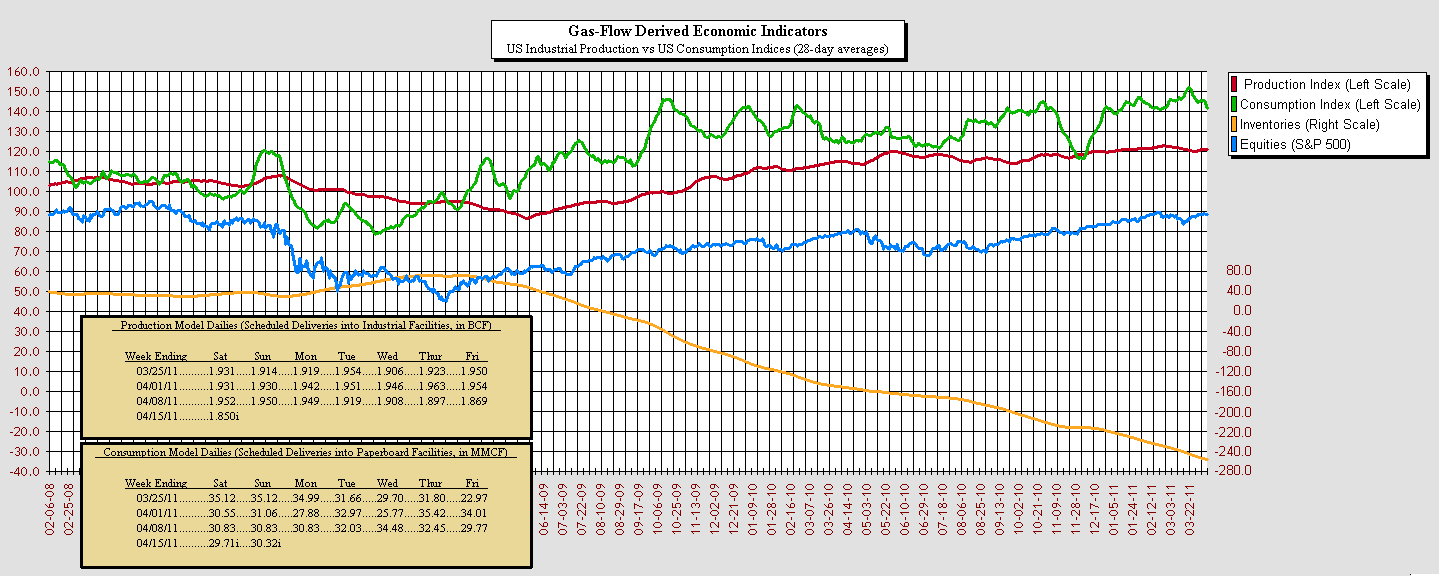

The US Industrial economy gained a little more ground last week (if pipeline scheduling is correct), while consumer spending continued to give back gains.

The US Industrial economy gained a little more ground last week (if pipeline scheduling is correct), while consumer spending continued to give back gains.The Production Index (In terms of its 28-day moving average of gas-flow scheduling into US industrial facilities) gained for it's second week in a row, advancing 121.3 (vs last weeks revised 120.9). In its dailies (raw, non-seasonally adjusted flows) the week started off strongly, but softened as the week progressed..

The Consumption Index continued lower (third down-week in a row), dipping to 141.9 (from last weeks 145.5). In its dailies the week started somewhat firm, strengthened through Wednesday, then declined through to the weekend.

The Inventories measure (the cumulative weekly difference between the Production Index and the Consumption Index) again continued in its long-term decline.

Overall, the recovery continues to appear strongly supported by elevated consumer-spending, an uncharacteristically-large lead in the Consumption Index over the Production Index, and continuing declines in the Inventories measure.

First-quarter results (due out starting in another weeks) look to be exceptionally strong, as large gaps (in the past) of consumption over production have generally been consistent (in the modeling) with large jumps in profitability. And that gap widened at the end of the quarter... probably to add to optimism as CEO's prepare their comments toward the 2nd quarter.

-Robry825